Salary Sacrifice: Transforming HR in 2025

As the workforce landscape continues to evolve, HR professionals face growing challenges to deliver benefits that are cost-effective, competitive, and engaging. Salary sacrifice—a tax-efficient method ...

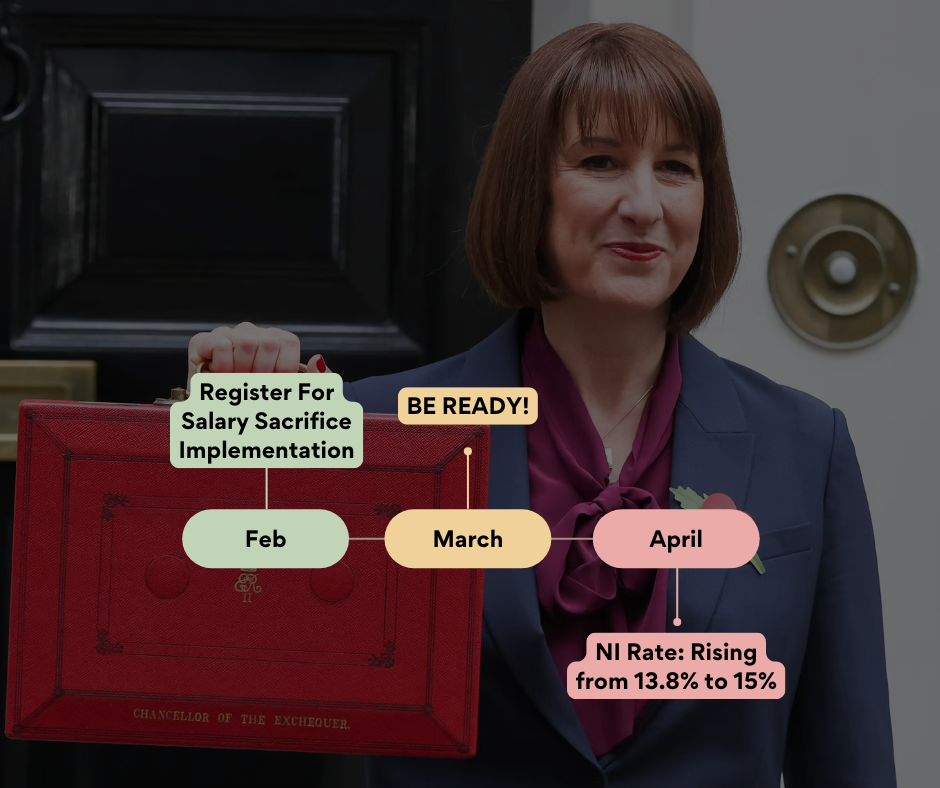

Be Ready: Higher Employer NI Rate in April 2025

With the Employer NI Rate set to rise from 13.8% to 15% in April 2025, alongside a lowered NI threshold, businesses face sharply increased payroll ...

Why Director-Only Companies Should Consider Workplace Pensions

Workplace pensions aren’t just for employees – they can be a smart financial move for directors too. Even if auto-enrolment (AE) rules don’t require you ...

Salary Sacrifice: Transforming HR in 2025

As the workforce landscape continues to evolve, HR professionals face growing challenges to deliver benefits that are cost-effective, competitive, and engaging. Salary sacrifice—a tax-efficient method ...