SAVE TIME. SAVE MONEY

Pension setup and management

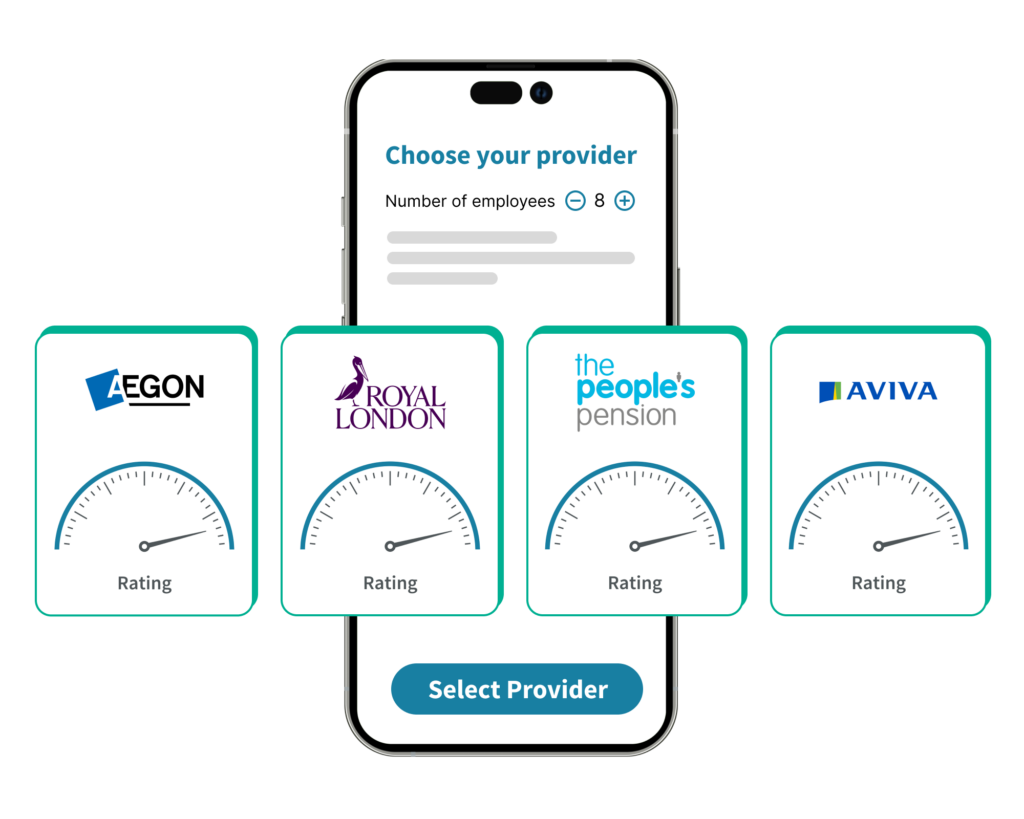

At Husky we deal with anything to do with workplace pensions for our clients, automating the entire process whilst ensuring compliance. With Husky, you gain access to preferential rates from the pension providers, potentially saving up to 80% on fees, and Husky sets it all up on your behalf.

EVERYONE WINS

We unlock the benefits of Salary Exchange

It allows you and your employees to save on National Insurance contributions, putting more money in their pockets each month and increasing cash savings for your business.

These savings generated can cover Husky’s fees, creating a win-win situation for everyone involved.

ALL IN ONE PLACE. DONE RIGHT.

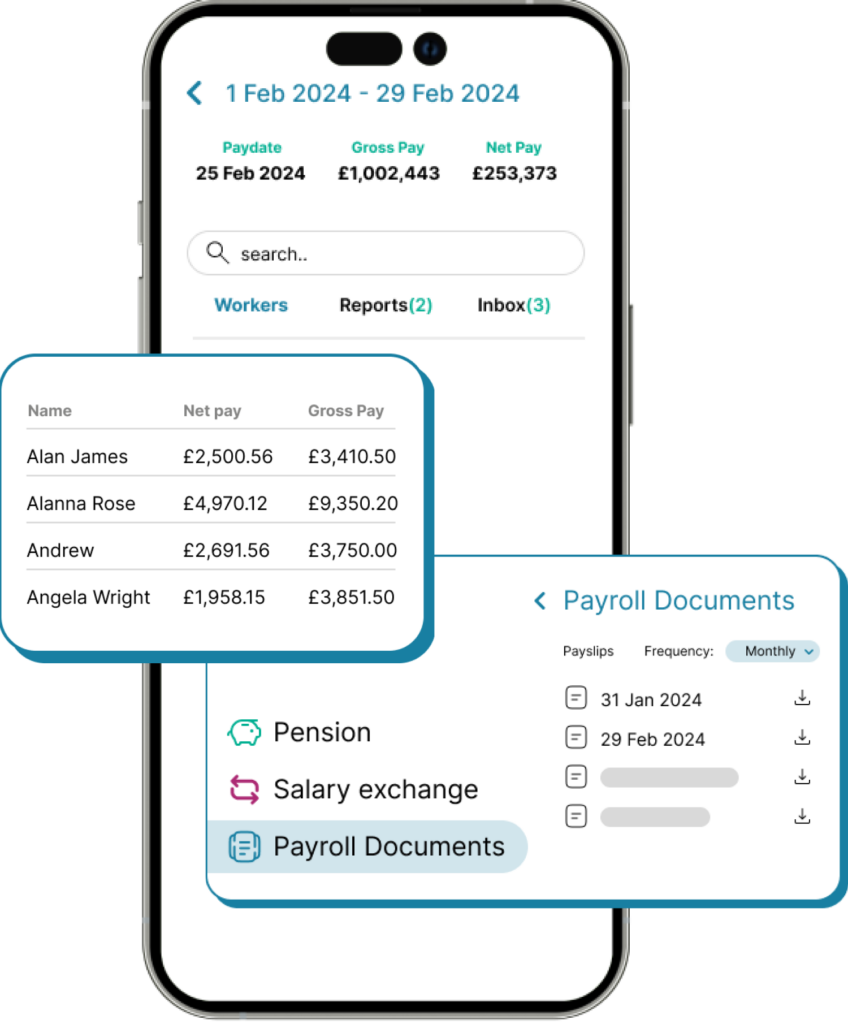

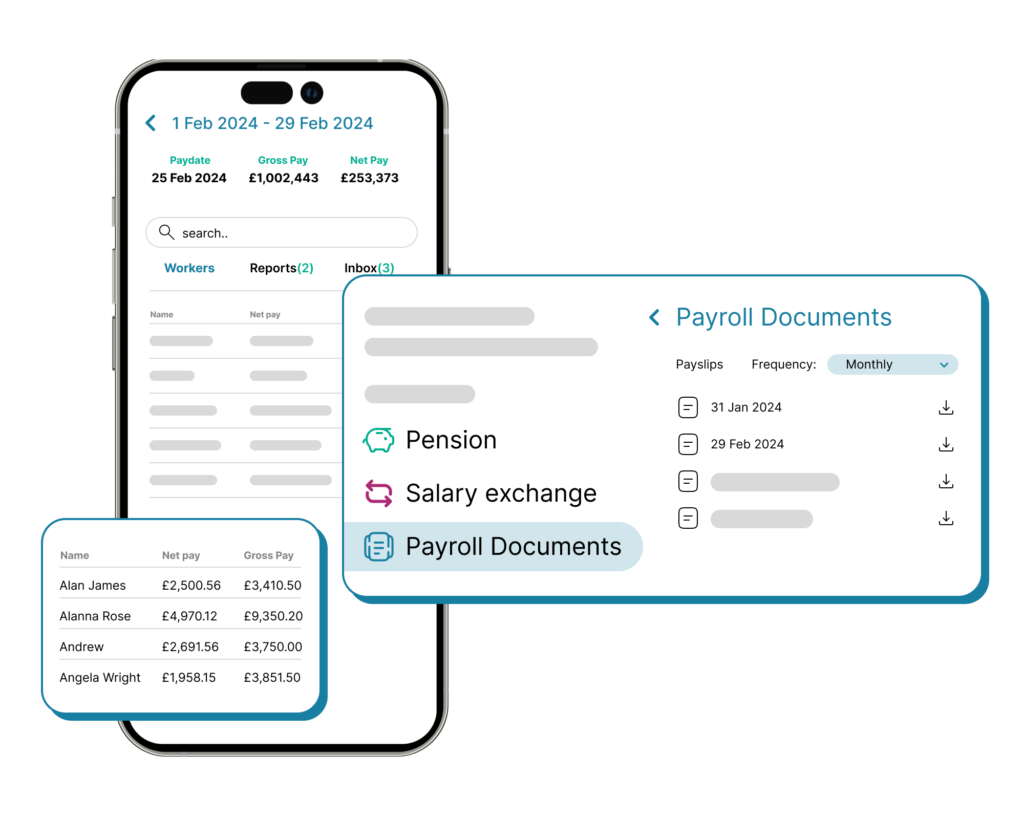

Simplified payroll solutions

Husky seamlessly manages your payroll and integrates with your existing pension schemes, all while utilising Salary Exchange for added savings. Our user-friendly app automates the whole workflow saving you time and money, and ensuring maximum efficiency and compliance. All the management is available in the portal for the employer as well.

BE COMPLIANT. NOT CONFUSED

Compliance made easy

We ensure all auto-enrolment obligations are met, rectify any existing issues, and maintain full compliance for every employer. Even if you have compliance issues or have received a notice or fine from The Pensions Regulator, Husky can always help. With a proven track record of managing compliance for over 2,000 businesses, we’ve saved our clients more than £50,000 in fines, reducing hassle and costs while ensuring peace of mind for your business.

Watch this video for a deeper understanding of Husky.

EXCELLENTTrustindex verifies that the original source of the review is Google. Professional responsive service that works for our business needs. Reliable, transparent, honest company to work with. Highly recommend.Posted onTrustindex verifies that the original source of the review is Google. My business, Spalding Massage Therapy used Husky's services throughout our period of employing staff. From set up and registering with HMRC through to sadly the point where we have had to stop employing, Husky and our point of contact Olga have been so helpful & professional. Their fees for small businesses are very reasonable IMHO and the Helpdesk has been relentlessly supportive - even when Olga had to explain the same thing to me 3 months running!Posted onTrustindex verifies that the original source of the review is Google. When time was of the essence Husky pulled our very new to the world of employment out of the waters. They were fast acting, professional and explained everything in a way that just melted all the anxiety of payroll and pensions away. The team are friendly and relatable, while being efficient and professional. We couldn't have asked for more, (a quick mention that Steve from payroll has been especially helpful and has gone above and beyond to explain any queries)Posted onTrustindex verifies that the original source of the review is Google. A very professional, efficient, trustworthy, reliable payroll and pension roll service provider that are competitively priced. Earl Shilton Town Council hope to have a long and happy working relationship with Husky Finance colleagues.Posted onTrustindex verifies that the original source of the review is Google. I would highly recommend Husky finance, I use them for Pensions on a number of our Companies. Kay is a superstar, she has helped me no end, a true professional throughout. Thank you Kay and all the team at Husky.Posted onTrustindex verifies that the original source of the review is Google. Excellent friendly service to sort all the statutory auto enrollment requirements in the UK for Erris Resources plc and Erris Gold Resources Ltd.Posted onTrustindex verifies that the original source of the review is Google. Husky manage both our monthly payroll and pension needs. From the beginning, they have been incredibly supportive. Our Head Office is in Ireland, so having a team knowledgeable of the intricacies of UK payroll and pensions has been a life saver for us.Posted onTrustindex verifies that the original source of the review is Google. Makes workplace pensions so much easier and transparentPosted onTrustindex verifies that the original source of the review is Google. We are certainly not their largest client, but they treat us so well and offer such great customer service, that you would think we were the most important client to them. Everything about working with Husky was so easy. We are a US based non profit hiring our first employee in the UK, so naturally, we had lots of questions. The team at Husky (especially Nigel and Kay) walked us through all of our options and really helped us find the best solution. I'd definitely recommend them.Posted onTrustindex verifies that the original source of the review is Google. We have used the services of Huskey for over a year now, they look after our company pension scheme. The reason I chose Huskey was because from the moment I contacted them they were so helpful and everything they promised, they followed through. Nothing was too much work for them. I would definitely recommend them.

Over 2,000 employers save time and money with Husky.

Award-winning solution

Gain some valuable insights

Salary Sacrifice: Transforming HR in 2025

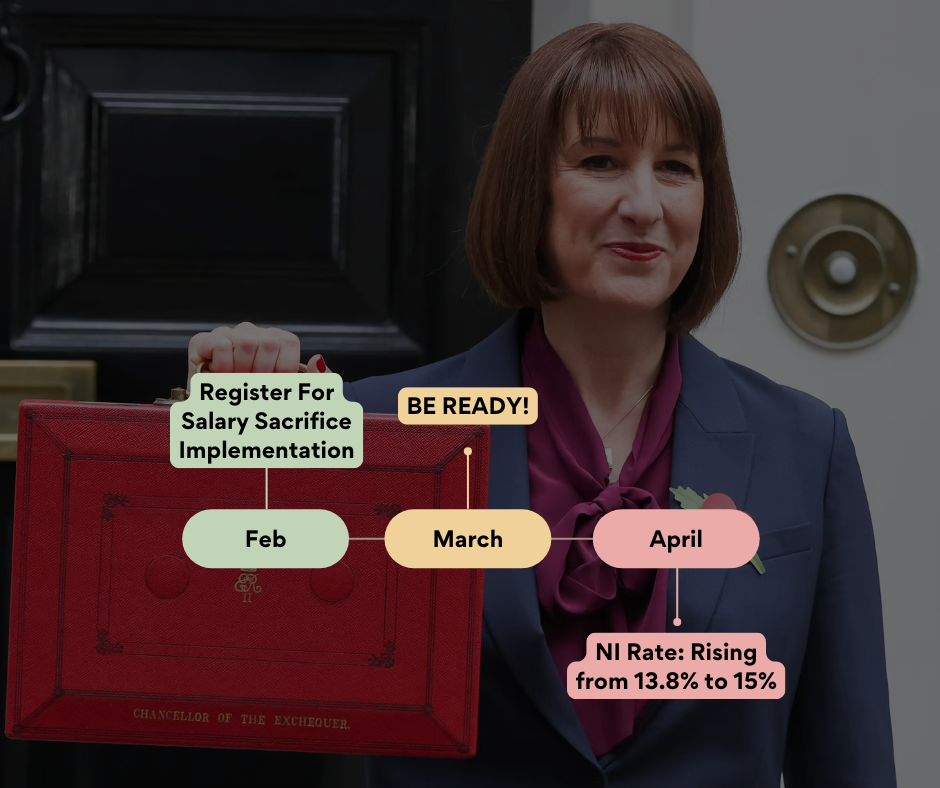

Be Ready: Higher Employer NI Rate in April 2025

Why Director-Only Companies Should Consider Workplace Pensions

Here are the frequently asked questions

If you have more questions you can always access our knowledge base on this link.

When should new employees be enrolled?

Employers must automatically enrol all new and eligible employees who are:

- aged 22 to state pension age

- earning over £10,000 a year

- Working or ordinarily work in the UK

- Not already part of a qualifying workplace pension scheme

Do I need to enrol overseas workers?

For Auto-Enrolment (AE) purposes, an employer only needs to assess and enrol UK workers into a scheme. Therefore, as an employer, you need to assess if a worker is working or ordinarily works in the UK under their contract.

Working in the UK: If a worker works wholly in the UK, then they can be considered to be working in the UK. By working wholly in the UK, The Pensions Regulator means:

- the worker’s contract provides for the worker to be based at a location in the UK, and the worker does, in practice, work all the time in the UK, and

- there is no simultaneous employment relationship between the worker and an employer outside the UK (e.g. the worker is not someone who has been sent to the UK by an affiliated employer, for example on a secondment.)

Ordinarily working in the UK: Where a worker is not wholly working in the UK (the work they do is also done outside of the UK), it will need to be established if the worker ordinarily works in the UK.

In most cases, workers who fall into this category will be workers who do not have one fixed workplace (for example, they move around in their work). To decide if a worker ordinarily works in the UK, an employer needs to consider:

- If the worker is resident in the UK

- where the worker begins and ends their work

- where the worker's headquarters in

- whether they pay NI and or tax in the UK

- the currency they are paid in

- the worker's contract of employment

- seconded workers

More details can be found here.

If you have a worker that should be exempt from AE due to not working in the UK, please enter that into Husky's system so that the worker is not assessed for Auto-Enrolment.

What does Qualifying Earnings mean?

- Jon earns £5,000 a month and contributes 5% into his pension and his employer contributes 3%

- His monthly qualifying earnings would be £3,669.00 (£4,189 - £520)

- Therefore, his pension contributions will be calculated as 5% of £3,669 and his employer contributions will be calculated as 3% of £3,669

You can find more details on how your pension contributions are calculated by logging into the Husky for Everyone app.

Can Salary Exchange be used with existing pension plans?

Yes, salary exchange can be introduced into an existing plan as well as new plans.

Can a salary exchange agreement be altered?

A salary exchange agreement can normally be altered, for example, if someone opts out of an automatic enrolment scheme with salary exchange.

For any other circumstances, it depends on how the agreement has been set up. It may be necessary to change the terms of a salary sacrifice arrangement where a lifestyle change significantly alters an employee’s financial circumstances.

This may include:

- changes to circumstances directly arising as a result of coronavirus (COVID-19)

- marriage

- divorce

- partner becoming redundant or pregnant

What are the benefits of a Salary Exchange scheme?

- Employers save on NI contributions while employees can save on tax as well as NI contributions.

- Employers can reinvest any NIC savings in their business or their employees’ pension plans.

- Employees receive a higher pension contribution or take-home pay, depending on how the arrangement’s set up.

- Employees can benefit from a bigger retirement fund, if NIC savings are reinvested back into their plan.

Are there any possible drawbacks to a Salary Exchange scheme?

- Lower life cover (employers generally calculate entitlement as a multiple of salary which would be lower)

- Lower borrowing available on mortgages (as per life cover the borrowing level is determined by a multiple of a lower salary)

- Entitlement to state benefits eg Statutory Maternity Pay and the State Pension may be affected if your salary falls below the level at which you pay National Insurance contributions.

- The employee might not be able to revert to their old (pre-sacrifice) salary if personal circumstances change. The employer would have to agree to a further change to the employee's contract of employment.

Those savings can be re-invested into the employee’s workplace pension pot to provide an even better employee benefit and encourage them to join. With Husky, you can also split those savings into specific %s so you can share the savings between the company and the employee.

Will Salary Exchange affect my current entitlement to Tax Credits?

You should speak to your tax credits office before you decide whether to participate in a Salary Exchange Scheme. You must also notify your tax credits office once you have exchanged your salary.

However, in broad terms, as your gross salary reduces (and employer pension contributions are disregarded) your entitlement to tax credits may increase. If you currently make personal contributions to a pension scheme, then you are currently entitled to deduct the gross amount of the pension contribution from your earnings to calculate your tax credits. In this situation, therefore, there should be little or no change to your tax credits entitlement.

How can one leave a salary exchange scheme?

Leaving a salary sacrifice exchange is always an option, and you should be able to do so without penalty if the arrangement isn’t working for you.