Why Director-Only Companies Should Consider Workplace Pensions

Workplace pensions aren’t just for employees – they can be a smart financial move for directors too. Even if auto-enrolment (AE) rules don’t require you to set one up, pensions offer significant benefits such as tax savings, reduced corporation tax, and long-term financial security.

Written by: Gustavo Fonseca

Are You Exempt from AE Duties?

No Employment Contracts: If you and other directors don’t have employment contracts, your company isn’t classified as an “employer” under AE rules. No pension or compliance duties apply.

One Director with a Contract: Still no AE duties – you don’t need a pension scheme or Declaration of Compliance (DOC).

Two or More Directors with Contracts: AE rules apply, and you’ll need to submit a DOC. You can choose whether to enrol or let directors opt in.

Even when AE doesn’t apply, setting up a pension is worth considering for the financial perks.

Why Set Up a Pension Anyway?

Contributing to a pension saves money and builds a secure future:

Corporation Tax Savings: Contributions are a business expense, reducing your taxable profits.

Income Tax and NI Savings: Pensions lower your personal and business tax liabilities.

Retirement Growth: Contributions grow tax-free and benefit from compound interest over time.

Brendan Shanks, Director of Husky, explains:

“Many directors don’t realise the immense tax benefits of contributing to a workplace pension. By diverting a portion of profits into a pension, they’re not just building for the future – they’re saving thousands in corporation tax today.”

Alex’s Story: The Director Who Future-Proofed His Finances

Alex, a 45-year-old sole director, avoided pensions to reinvest in his business. Then, his friend Rachel shared how her workplace pension grew to £220,000 after years of small, tax-efficient contributions. Alex decided to act, contributing £10,000 annually. He now saves thousands in taxes and is building a robust retirement pot.

Olga Sala, COO of Husky adds:

“Stories like Alex’s are so common. Directors often overlook pensions, thinking it’s an unnecessary expense. But once they see the numbers and the tax savings, it becomes clear it’s one of the smartest moves they can make.”

Why Choose Husky for Your Workplace Pension?

At Husky, we handle everything related to workplace pensions for you, automating the process and ensuring compliance. Here’s why directors trust us:

Save up to 80% on fees: Use our comparator tool to access preferential rates from providers such as Aviva, People’s Pension, etc.

Full Setup and Administration: Husky sets up your pension and manages it for you, auditing each payroll and liaising with The Pensions Regulator to reduce compliance liability.

Engagement Tools: The Husky4Everyone app helps you stay engaged with pensions.

Salary Exchange Support: We simplify salary exchange, handling setup and administration to maximise tax and NI savings.

Take Action Today

Setting up a workplace pension isn’t just about compliance – it’s a smart way to save money and build financial security. With Husky, it’s easier and more cost-effective than ever. Let us handle your workplace pension so you can focus on growing your business.

Start now and future-proof your finances with Husky.

Get more now. Have more later.

We setup and manage your pensions, payroll, and salary exchange—all in one place, ensuring compliance every step of the way.

For many employees, changes in their net pay can be perplexing and sometimes concerning. Net pay, or the amount received after deductions and taxes have been subtracted from gross pay, can fluctuate due to various factors. Understanding why your net pay may have changed is essential for financial planning and peace of mind. Here are some common reasons why your net pay may have changed.

May 7, 2024

Navigating Payroll. Understanding P32 and How to Pay HMRC

May 1, 2024

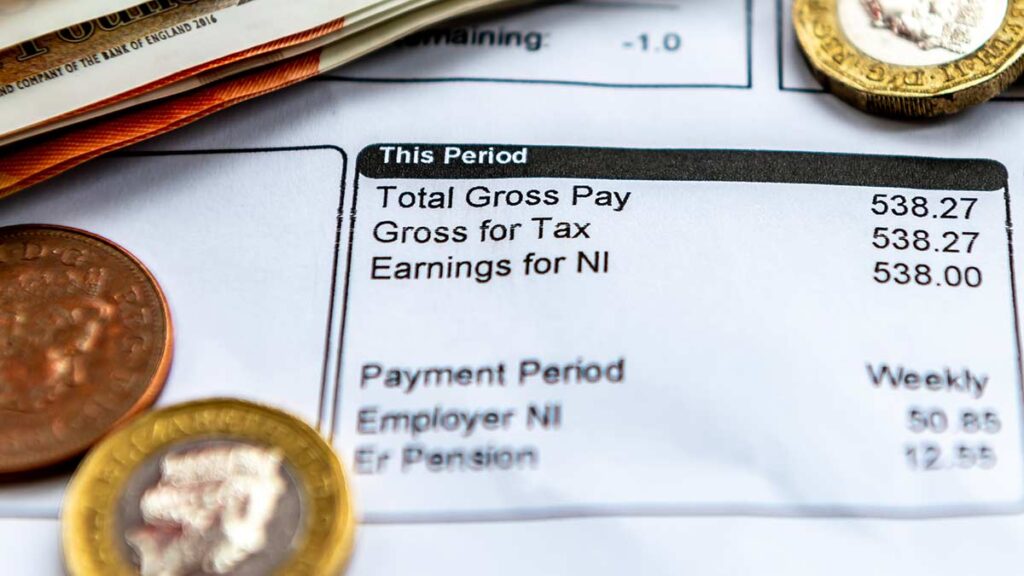

Understanding Your Payslip: How Payroll Works

December 20, 2023

2023-2024 National Insurance Contribution Rate Cut: What You Need to Know

June 30, 2023

Don’t Let Your Payroll Software Dictate Your Workplace Pension Choices

June 26, 2023

Outsourcing payroll with Husky Finance: what you need to know